Principal & interestOwner-occupier 10% min. Deposit

5.99%

interest rate

6.51%

comparison rate

What you need to know

The lowest rate on the market right now is 5.69%.

You could save $8,856 a year by switching to the cheapest variable rate.

The cheapest rate might not be the best loan: look out for fees and features, and remember you might end up with a higher rate if you want to borrow above 80% of the property value.

{"isComparisonEngineEnabled":true}

{"userFilters":[{"componentType":"MULTI-SELECT CHECKBOX","options":{"comparator":"contains","includeAllSelection":false,"defaultMatcher":"ANY","values":["Owner-occupier","Investor"],"fields":[{"label":"Owner-occupier","value":"Owner-occupier","comparator":"contains"},{"label":"Investor","value":"Investor","comparator":"contains"}]},"dataSelector":{"recordType":"VARIANT","fieldCode":"DETAILS.LOAN_PURPOSE"},"dataType":"TEXT","label":"Loan Purpose","order":0},{"componentType":"MULTI-SELECT CHECKBOX","options":{"comparator":"contains","includeAllSelection":false,"defaultMatcher":"ANY","values":["Fixed","Variable"],"fields":[{"label":"Fixed","value":"Fixed","comparator":"contains"},{"label":"Variable","value":"Variable","comparator":"contains"}]},"dataSelector":{"recordType":"PRODUCT","fieldCode":"DETAILS.PRODUCT_TYPE"},"dataType":"TEXT","label":"Loan type","order":1},{"componentType":"MULTI-SELECT CHECKBOX","options":{"comparator":"contains","includeAllSelection":false,"defaultMatcher":"ANY","values":["5","10","20","30","40"],"fields":[{"label":"less than 5%","value":"5","comparator":"lte"},{"label":"10%","value":"10","comparator":"eq"},{"label":"20%","value":"20","comparator":"eq"},{"label":"30%","value":"30","comparator":"eq"},{"label":"40% or more","value":"40","comparator":"gte"}]},"dataSelector":{"recordType":"VARIANT","fieldCode":"DETAILS.MIN_DEPOSIT"},"dataType":"PERCENTAGE","label":"Min. deposit","order":2},{"componentType":"SINGLE-SELECT CHECKBOX","options":{"fields":[{"label":"Offset account","fieldCode":"FEATURES.MORTGAGE_OFFSET","value":1},{"label":"Redraw facility","fieldCode":"FEATURES.FACILITY_REDRAW","value":1},{"label":"Extra repayments","fieldCode":"FEATURES.EXTRA_PAYMENTS","value":1},{"label":"Cashback","fieldCode":"GENERAL.CASHBACK","value":1},{"label":"Finder award winner","fieldCode":"GENERAL.FINDER_AWARDS_WINNER","value":1}]},"dataSelector":{"recordType":"VARIANT","fieldCode":null},"dataType":null,"label":"Features","order":3},{"componentType":"PROVIDER","options":null,"dataSelector":{"recordType":"PRODUCT","fieldCode":"GENERAL.PROVIDER_ID"},"dataType":"UUID","label":"Lender","order":4}],"niche":{"currencySymbol":"$","decimalPoint":".","decimalPlaces":"2","thousandsSeparator":","},"prefilled":false}

These home loans offer low costs, coupled with a host of features, giving the best overall value.

7+

Great

These home loans may have slightly higher interest rates or fewer features but overall, a competitive offering.

5+

Standard

Usually the home loans would offer above average rates. They may still include some competitive features.

0+

Basic

Higher costs and/or fewer features.

The products compared on this page are chosen from a range of offers available to us and are not representative of all the products available in the market. There is no perfect order or perfect ranking system for the products we list on our site, so we provide you with the functionality to self-select, re-order and compare products. The initial display order is influenced by a range of factors including conversion rates, product costs and commercial arrangements, so please don't interpret the listing order as an endorsement or recommendation from us. We're happy to provide you with the tools you need to make better decisions, but we'd like you to make your own decisions and compare and assess products based on your own preferences, circumstances and needs.

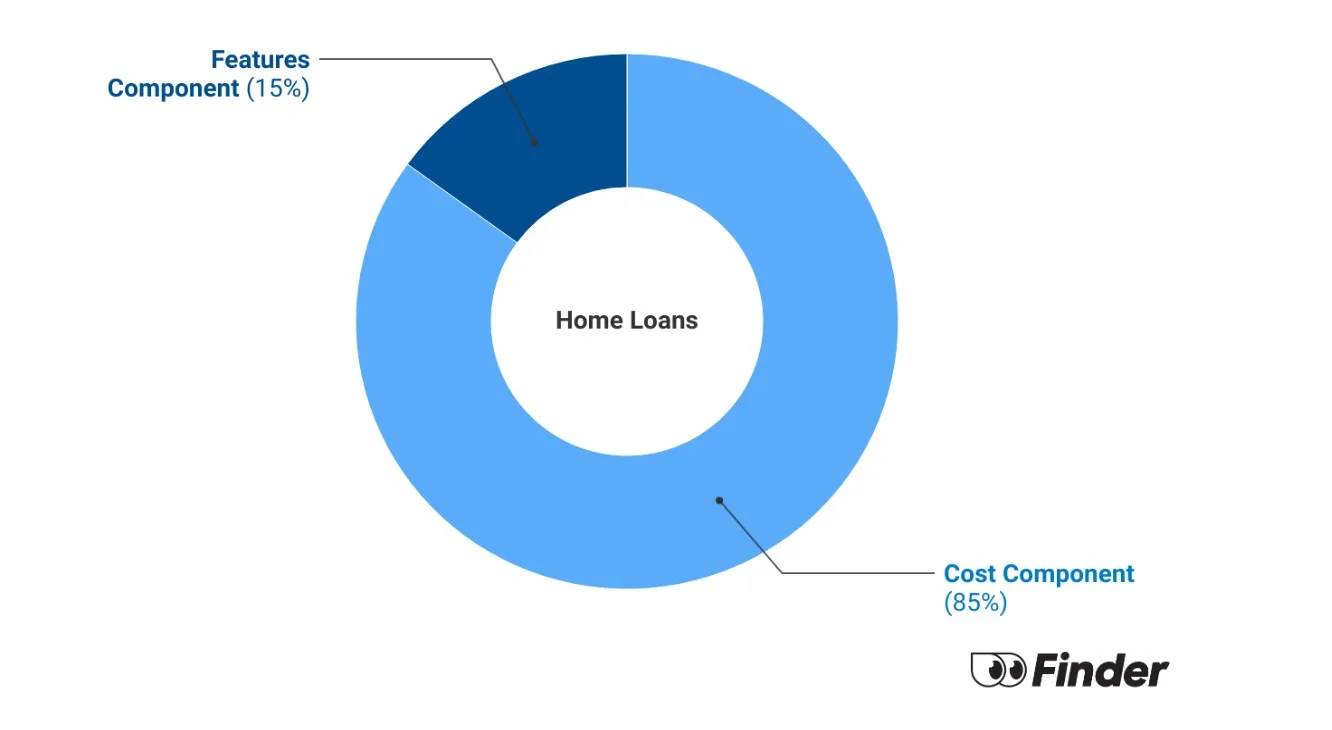

What is Finder Score?

The Finder Score crunches 7,000 home loans across 120+ lenders. It takes into account the product's interest rate, fees and features, as well as the type of loan eg investor, variable, fixed rate - this gives you a simple score out of 10.

To provide a Score, we compare like-for-like loans. So if you're comparing the best home loans for cashback, you can see how each home loan stacks up against other home loans with the same borrower type, rate type and repayment type. We also take into consideration the amount of cashback offered when calculating the Score so you can tell if it's really worth it.

We put every effort into ensuring information on Finder is accurate. This article was reviewed by John Pidgeon from our Editorial Review Board as part of our fact checking process.

How to compare the cheapest home loan rates

You’d think it was as simple as looking at the lowest number in the table, right? Well, it can be. But there are some things to watch out for that could make your cheap home loan…not so cheap.

1. Ok yes, look at the rate

The starting point is to always look at the rate. The lower rate, the lower your repayments.

2. But then look at the fees

Some loans lure you in with a cheap attractive rate, but then you find it piles on a huge fee to apply and another fee to pay each month as well. Your cheap rate now costs you more per month than the slightly higher interest rate with no fees.

3. Then have a little glance at the comparison rate

Comparison rates are normally based on loans of $150,000 so they’re not always helpful. But if the comparison rate is much higher than the actual interest rate, you can bet there are other costs driving your repayments up.

4. Don't forget to look at the features

It’s all well and good getting a low interest rate but if you’re sacrificing access to features that could save you money in the long run, it’s not worth it. Take an offset account, for example. Using an offset account will mean you pay down the loan faster because it reduces the amount of interest you need to pay.

The lower the interest rate the lower the repayments

The number one factor in determining a cheaper home loan is a low interest rate.

Let's compare 2 otherwise identical home loans with slightly different interest rates.*

Interest rate

7.48%

5.69%

Loan amount

$626,052

$626,052

Loan term

30 years

30 years

Monthly repayment

$4,369

$3,630

Monthly saving

N/A

$739

Annual saving

N/A

$8,868

As you can see, with the lower interest rate, you save $739 a month – or $8,868 a year.

*We're using the average owner-occupier home loan size from the ABS, the average variable rate loan in Finder's database of the full market and the lowest variable rate.

What are the lowest home loan rates on the market?

Every month, we analyse the rates in our database to create a list of the market's cheapest loans.

The lowest variable interest rate in Finder’s database is 5.69%

The lowest fixed interest rate in Finder’s database is 5.59%

The cheapest rates over time.

Every month, we find the lowest home loan rates in our database for 4 different loan types. To ensure these products are not overly restrictive in eligibility criteria, every loan we select must meet the following criteria:

Loans must be principal and interest loans with a maximum LVR of 80%, meaning you need a minimum 20% deposit.

Fixed rates have terms of between 1 and 5 years.

Mortgages are taken from Finder's database, with rates correct at the time of publication (updated every month).

What are the cheapest home loans at the big 4 in August 2024?

Interest rates can change depending on your circumstances, but as a guide, here are the cheapest home loans from the big 4.

The cheapest variable rate from the big 4 is from CBA's new digital home loan which launched in May 2024. Even so, it's a considerable difference from the lowest variable rate across the market.

As a sign of what could be to come, in July NAB dropped its fixed rate to be the only Big 4 bank below 6%.

Let's do what we do best: compare.

Say you take out a $500,000 loan over 30 years with that 6.15% rate. You'd be paying $3,047 a month in repayments.

But with May's lowest variable rate across the market of 5.69%, you'd only (ha) be paying $2,899. That's a difference of $148 a month, or $1,776 a year.

Your repayments with NAB's lowest rate of 5.99% would be $2,995 per month - but remember that you'd be locked into that rate even if rates start dropping.

Your interest rate update

On 18 June the official cash rate was held at:

4.35%

The lowest variable owner-occupier rate on the market is:

5.69%

Assuming the average owner occupier home loan size of $626,052 you would be making monthly repayments of:

$3,630

I wanted to make sure I have one of the cheapest home loans on the market. So I found an online lender with a consistently low interest rate (I should know, I check rates every month). But I also made the sure the loan had an offset account. For me, being able to build up savings in the offset account speeds up my loan and cuts down my overall interest charges dramatically. This makes the loan much cheaper in the long run.

At a very basic level, the cheapest home loan is the one with the lowest rate. But every borrower has different needs. So beyond a low rate, you need to get a loan that actually helps you achieve your property goals and financial needs.

A loan you can pay off asap

Home loans are normally taken out for 30 years. But no one wants to spend the next 30 years making those repayments, right? With most variable rate home loans you can actually make extra repayments. By paying more off your loan than the required monthly repayments, you pay off the loan early and pay less in interest.

Fixed rate loans are less likely to allow extra repayments and will probably charge a break fee if you do repay early.

A loan that matches your strategy

Owner-occupier home loans have the cheapest rates. But they're no good if you're a property investor because you'll need an investment loan.

Most borrowers want a principal and interest loan, but for investors, an interest-only loan offers tax benefits. It’s important to understand your strategy early on. You may be someone that will start off as an owner occupier but then move out and use it for investment (if you have taken advantage of first home owner concessions, for example).

A loan with an offset account

Is it worth going for the cheapest home loan if it doesn't have an offset account?! Well, that's up to you. But considering an offset account could see you paying your loan off early and therefore less in interest, it's a pretty key thing to want to include as part of your loan. An offset account is essentially a bank account attached to your mortgage. Instead of earning interest, it reduces the interest you'll pay.

Let's say you have $100,000 in your offset account and you have a $500,000 loan. You'll only pay interest on $400,000.

You still repay the same amount every month, but this just means more of your repayment goes towards the remaining loan value and not on interest. So you end up finishing the loan faster.

If I had to credit just one thing with helping me repay my home loan in just 7 years, I'd say it was an offset account. This is a debt-busting secret weapon. You should keep every cent to your name in one of these – we're talking your savings for everything, your emergency cash stash and even your salary. You'll likely save tens of thousands of dollars and shave years off your time in debt.

3 extra tips to help you save money on your home loan

1. Choose your loan term carefully

Most borrowers choose 30-year loan terms. And spread out over that time, your monthly repayments are as low as possible.

If you picked a shorter loan term your monthly repayments would be higher, but you'd pay off your loan 5 years earlier, saving thousands in interest.

Let's look at 3 examples. These loans are all for the same amount borrowed, but the loan term changes:

Loan term

30 years

25 years

20 years

Interest rate

6.00%

6.00%

6.00%

Loan amount

$600,000

$600,000

$600,000

Monthly repayment

$3,598

$3,866

$4,299

Total cost*

$1,295,030

$1,159,743

$1,031,611

*Total cost here refers to the amount of interest you pay over the life of the loan, plus the principal.

As you can see, a longer loan term means cheaper monthly repayments. But a shorter loan means you pay less interest in the long run, making the whole loan cheaper.

2. Find a loan with lower fees

Some lenders charge multiple loan fees that can add up to hundreds of dollars. But other lenders charge basically no fees at all (you still have to pay government fees like a mortgage registration fee).

If 2 loans have identical interest rates and features, the one with fewer fees will be the cheapest home loan.

3. Save a bigger deposit

Easier said than done, of course. But saving a bigger deposit means borrowing less money. And that instantly makes your home loan cheaper.

It saves you money in other ways too:

You can avoid lenders mortgage insurance. If your deposit is at least 20% of your property's value, you can avoid the added expense of lenders mortgage insurance (LMI). Borrowers with smaller deposits usually have to pay this, which can add thousands of dollars to your loan costs.

You can unlock lower rates. Many lenders reserve their cheapest interest rate offers for borrowers with a deposit of 20% or more.

Watch: How to find a lower home loan rate

Why you can trust Finder's home loan experts

You pay nothing. Finder is free to use. And you pay the same as going direct. No markups, no hidden fees. Guaranteed.

You save time. We spend 100s of hours researching home loans so you can sort the gold from the junk faster.

You compare more. Our comparison tools bring you cheaper, better home loans from across the market.

Frequently asked questions about getting a cheap home loan

Some of the market's cheapest home loans come in the form of special discount rate offers. These loans offer a cheap rate to entice you in but revert to a higher rate after a year or two.

Let's be clear, there's nothing bad about these deals. A low rate is a low rate. You just need to pay attention to the interest rate once the discount period ends and refinance to a better loan if your new rate jumps up. But every borrower needs to watch their rate, as lenders do move rates up and down (or keep you on your current rate while offering cheaper home loans to new customers!).

Also look at discharge or exit fees. You don't want to get hit with a big fee when trying to exit the loan later (although a small fee isn't so bad if the rate is very competitive).

Right now, variable rate loans are a little higher than fixed rate loans. This is a sign of the times and not always the case. If you look at the table on this page which shows the big 4 banks' lowest interest rates, you can see there's a mix.

Online lenders, fintechs and small digital banks tend to have cheaper home loan rates than bigger banks. If you're not comparing rates from these lenders, you might miss some of the best deals on the market.

Mortgage brokers are great at helping you find a home loan and handling mortgage paperwork. But they often don't have small online lenders in their panel of lenders, so you might miss out on a very low rate.

it's a myth that the Big Four always have much higher rates. It's a very competitive market. There's often not much difference between a hot online deal and a big bank's lowest variable rate.

Many of the cheapest loans among Finder's partners (and the wider market) are from smaller banks and local credit unions. But banks are changing their rates and policies constantly, and the Big 4 can be low as well. This is why you really have to compare as many lenders as you can.

Some lenders offer special loans tailored to first home buyers that are worth checking out. You can use our comprehensive guide to learn more about getting a loan as a first home buyer.

Mortgage brokers compare loans for you and are experts at helping borrowers find appropriate products. If you're confused or need help, a broker can be very useful.

But you should also know that many of the market's lowest rates (including many listed on this page) are offered by small lenders that don't appear in a mortgage broker's panel. If the lender isn't in the broker's panel, they cannot help you.

But brokers are helpful for other reasons, and if you have more concerns than just finding the absolute lowest rate, then speaking to a mortgage broker is a good idea. Just do your own research as well.

Saving up for your home loan deposit is a serious challenge for everyone. However, there are ways to trim your expenses, build your deposit and find home loans that don't need large deposits. To master the art of saving for a home loan deposit, you should look at our in-depth, 6-part guide to home loan deposits.

You should always be comfortable with the lender you're planning on going with. If you're not aware of a lender, try calling it to find out about the company and its service level before lodging an application. Speak to previous customers or read customer reviews online.

Keep in mind that little-known lenders might be funded by a larger bank, as is the case with NAB-backed UBank or Firstmac-backed loans.com.au.

John is the co-host of the this is money and this is property podcasts (formerly my millennial money and my millennial property). He is Director at SOLVERE Wealth, Director/Buyers Agent at Envisage Property, and is property coach of over 25 years.

Richard Whitten is a money editor at Finder, and has been covering home loans, property and personal finance for 6+ years. He has written for Yahoo Finance, Money Magazine and Homely; and has appeared on various radio shows nationwide. He holds a Certificate IV in mortgage broking and finance (RG 206), a Tier 1 Generic Knowledge certification and a Tier 2 General Advice Deposit Products (RG 146) certification. See full bio

Richard's expertise

Richard has written 538 Finder guides across topics including:

Home loan cashback deals can help you refinance to a cheaper interest rate and get a lump sum cash payment. Compare the latest deals and check your eligibility today.

In the market for a home or investment? The right buyer's agent could save you thousands. Learn what a buyer's agent does, how much it will cost and more.

You can apply for one of the loans on this page by clicking the green button that says ‘Go to site’. Once you arrive at the lender’s site, you should have all the information you need to apply.

Cheers,

Sarah

rixSeptember 12, 2019

I have a house that is located in Perth WA and the mortgage is fixed for 2 more years. I would like to change to a lender that is offering less than 3% as the fixed rate of 4.5% can you advise me the safest way to go? mortgage is approximately $160,000 on a 3 year old new home 4 x 2

NikkiSeptember 13, 2019

Hi Rix,

Thanks for getting in touch!

You may refer to our complete guide to refinancing your home loan to know how to get started. You can also refer to our list of refinancing home loans to compare your options. Our table should allow you to compare the features and benefits of each loan provider such as max loan rate, interest and etc. This way it will be easier for you to see which provider fits you best. Banks like HUME, Virgin, and Ubank offer interest rates of less than 3%. If you need further help, a quick guide on how to compare home loans is also stated on the page.

A mortgage broker is the best person to reach out to see your options for refinancing. They can give you a multitude of options according to your situation. In the meantime, to give you an idea of how your monthly repayments will go, you may use our home loan calculator.

As a friendly reminder, carefully review the eligibility criteria of the loan before applying to increase your chances of approval. Read up on the terms and conditions and product disclosure statement and contact the bank should you need any clarifications about the policy.

Hope this helps and feel free to reach out to us again for further assistance.

Best,

Nikki

IanJuly 24, 2019

I have been looking into refinancing my property, but as it’s an acreage (60 ha), no lenders seem to be interested in me.

Finder

JeniJuly 24, 2019Finder

Hi Ian,

Thank you for getting in touch with Finder.

There are lenders from our rural or hobby farm home loans guide. You can compare your options using our comparison table. When you are ready, press the ‘Go to site’ button to apply. You can also seek professional help from a mortgage broker since you’re having a hard time finding the right bank/lender.

Before applying, please ensure that you meet all the eligibility criteria and read through the details of the needed requirements as well as the relevant Product Disclosure Statements/Terms and Conditions when comparing your options before making a decision on whether it is right for you. You can also contact the provider if you have specific questions.

I hope this helps.

Thank you and have a wonderful day!

Cheers,

Jeni

KeithApril 11, 2019

I have just paid off my house worth approx $800-850k. I am looking at ways besides dying to assist my two children into getting into a property. Can you expand on the family pledge home loan as they both have not got a deposit or another product in which I can assist with them getting into the property market?

Thanks.

Finder

JeniApril 13, 2019Finder

Hi Keith,

Thank you for getting in touch with Finder.

You can assist your kids to get a deposit together. For example, the child saves 5% or 10% of a property’s value, and the parent can use the equity in their house to cover the other 10-15%. The child pays back the whole loan (including the amount guaranteed by the parent). Once the parent’s part of the deposit is repaid by the child, the parent/guarantor is usually free from any other debt even if the child can’t repay the rest. But the big risk is if the child can’t repay the loan (including deposit) the parent/guarantor may have to repay it.

Please refer to our guarantor home loans guide for more details and to compare your options.

I hope this helps.

Thank you and have a wonderful day!

Cheers,

Jeni

Important information about this website

finder.com.au is one of Australia's leading comparison websites. We are committed to our readers and stands by our editorial principles

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product. You can learn more about how we make money.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

You pay nothing. Finder is free to use. And you pay the same as going direct. No markups, no hidden fees. Guaranteed.

You pay nothing. Finder is free to use. And you pay the same as going direct. No markups, no hidden fees. Guaranteed.

You save time. We spend 100s of hours researching home loans so you can sort the gold from the junk faster.

You save time. We spend 100s of hours researching home loans so you can sort the gold from the junk faster.

You compare more. Our comparison tools bring you cheaper, better home loans from across the market.

You compare more. Our comparison tools bring you cheaper, better home loans from across the market.

Hi. I just wanted to know is there any reason why Reduce home loans are no longer on your home loan comparison site ?

Hi Dash,

You can compare rates from Reduce home loans on this page.

I hope this helps.

Kind regards,

Richard

how can I get lown

Hi Hugo,

You can apply for one of the loans on this page by clicking the green button that says ‘Go to site’. Once you arrive at the lender’s site, you should have all the information you need to apply.

Cheers,

Sarah

I have a house that is located in Perth WA and the mortgage is fixed for 2 more years. I would like to change to a lender that is offering less than 3% as the fixed rate of 4.5% can you advise me the safest way to go? mortgage is approximately $160,000 on a 3 year old new home 4 x 2

Hi Rix,

Thanks for getting in touch!

You may refer to our complete guide to refinancing your home loan to know how to get started. You can also refer to our list of refinancing home loans to compare your options. Our table should allow you to compare the features and benefits of each loan provider such as max loan rate, interest and etc. This way it will be easier for you to see which provider fits you best. Banks like HUME, Virgin, and Ubank offer interest rates of less than 3%. If you need further help, a quick guide on how to compare home loans is also stated on the page.

A mortgage broker is the best person to reach out to see your options for refinancing. They can give you a multitude of options according to your situation. In the meantime, to give you an idea of how your monthly repayments will go, you may use our home loan calculator.

As a friendly reminder, carefully review the eligibility criteria of the loan before applying to increase your chances of approval. Read up on the terms and conditions and product disclosure statement and contact the bank should you need any clarifications about the policy.

Hope this helps and feel free to reach out to us again for further assistance.

Best,

Nikki

I have been looking into refinancing my property, but as it’s an acreage (60 ha), no lenders seem to be interested in me.

Hi Ian,

Thank you for getting in touch with Finder.

There are lenders from our rural or hobby farm home loans guide. You can compare your options using our comparison table. When you are ready, press the ‘Go to site’ button to apply. You can also seek professional help from a mortgage broker since you’re having a hard time finding the right bank/lender.

Before applying, please ensure that you meet all the eligibility criteria and read through the details of the needed requirements as well as the relevant Product Disclosure Statements/Terms and Conditions when comparing your options before making a decision on whether it is right for you. You can also contact the provider if you have specific questions.

I hope this helps.

Thank you and have a wonderful day!

Cheers,

Jeni

I have just paid off my house worth approx $800-850k. I am looking at ways besides dying to assist my two children into getting into a property. Can you expand on the family pledge home loan as they both have not got a deposit or another product in which I can assist with them getting into the property market?

Thanks.

Hi Keith,

Thank you for getting in touch with Finder.

You can assist your kids to get a deposit together. For example, the child saves 5% or 10% of a property’s value, and the parent can use the equity in their house to cover the other 10-15%. The child pays back the whole loan (including the amount guaranteed by the parent). Once the parent’s part of the deposit is repaid by the child, the parent/guarantor is usually free from any other debt even if the child can’t repay the rest. But the big risk is if the child can’t repay the loan (including deposit) the parent/guarantor may have to repay it.

Please refer to our guarantor home loans guide for more details and to compare your options.

I hope this helps.

Thank you and have a wonderful day!

Cheers,

Jeni