Finder makes money from featured partners, but editorial opinions are our own.

The best extras cover – we crunched 400 policies (yup, really)

Stop putting off that dental checkup with extras cover that has main character energy.

Who is this cover for?

No contact details required

Compare 40+ funds

Same price as going direct

Back

Close

I'm Tim, your insurance expert.

Here to help you find the right cover for you!

Step 1/2 - About your cover

Which state do you live in?

QLD

NSW

ACT

VIC

TAS

SA

WA

NT

What's your age?

Depending on your age, you may be eligible for an

aged-based discount. This is used to estimate your

rebate.

Under 65

65 - 69

70 or older

What's your household's taxable income?

This is the combined income you and your spouse earn before tax. It's needed to calculate the correct Australian government rebate.

$93,000 and under

$93,001 to $108,000

$108,001 to $144,000

$144,001 and over

What kind of health insurance do you need?

Combined (Extras + Hospitals)

Extras

Hospital

What level of hospital coverage would you like?

You can change this at any time later.

Legend

Covered

Restricted cover, You may be partially covered for

this category.

Not covered. Optional for insurer to include.

*Prices updated August 2024, in line with Finder's database of health insurance policies. Prices reflect the cheapest available for a single individual with less than $97,000 income and living in Sydney with a $750 excess.

What extras cover do you need? (Optional)

Select as many as you want or move to the next step

Preventative & general dental

Major dental & implants

Optical

Physiotherapy

Podiatry

Non-PBS pharmaceuticals

Chiropractic

Emergency ambulance

Remedial massage

Email me my results (optional)

To get a copy of your results for later, add your email below

Extras cover helps pay for non-hospital treatments like dental, optical, physiotherapy and more.

Most extras treatments are not covered by Medicare.

Extras cover starts at around $4 per week.

Extras cover explained

Extras cover helps pay for medical care that's not covered by Medicare. These treatments are usually done out-of-hospital and include dental, physio, psychology, optical and chiropractic services. You must serve a waiting period before you can claim money back and there are annual cover limits (a cap on how much you can claim per year).

Hospital only

Hospital cover helps pay for treatment and surgery in a private hospital.

Extras only

Extras cover helps cover the cost of optical, dental, physio and more.

Combined

Combined coverage includes hospital and extras coverage, each tailored to your needs.

Get cheap extras cover

Filter by price to find the cheapest extras policies available on Finder.

Each month we analyse over 10,000 hospital insurance products and rate each one on price and features. What we end up with is a nice round number that helps you compare hospital cover a bit faster.

9+ Excellent - Competitive pricing coupled with highly ranked extras.

7+ Great -Balanced pricing and features, offering overall good value.

5+ Satisfactory - These products offer a balance between price and features.

Less than 5 – Basic - These products usually offer fewer extras or above average pricing.

Pools and categories

We want to compare apples to apples, not apples to apple pie. It doesn't make sense to compare a top extras policy with coverage for hearing aids and braces against a policy designed only for dental. So we've separated all the extras policies on the market into pools and categories.

The Finder Score methodology is designed by our insights team and reviewed by our editorial team. Commercial partners carry no weight, and all products are reviewed objectively.

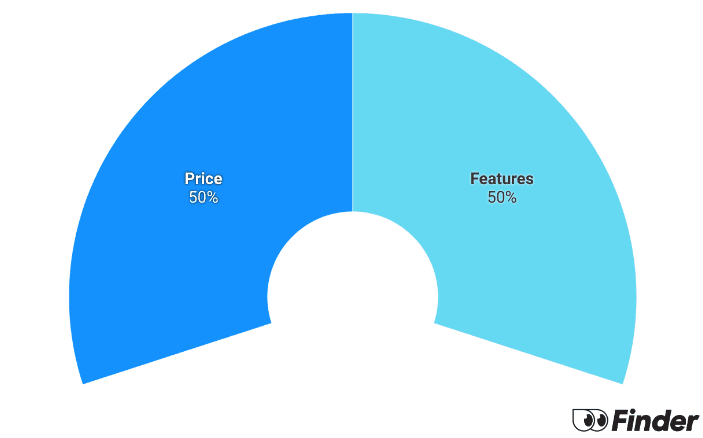

Once in their pools and categories, each product gets a Price Score and a Features Score, which are then combined to give the Final Score.

We've made 28 pools covering each state and lifestage. Each product is put into a pool, and can only be part of that 1 pool. This means each product is only compared against other products that make sense. Each pool has a unique combination of:

State - The state the policyholder resides in

Lifestage - Single / Single Parent Family / Couple / Family

With 7 states (Health Insurance is the same price in NSW and ACT) and 4 life stages, this multiplies out to the 28 pools. This process makes sure each product gets a score based on their position within a similar group of products.

Category: We also give each product a Category, depending on the number of extras that are provided. Extras that only cover Ambulance are excluded from receiving a Finder Score. The categories are Core, Medium and Comprehensive. Policies are only considered in the highest category they are eligible for.

Price Score

The monthly price for each product is compared against other products within its assigned product pool and category. Each product is assigned a score between 1 - 10, with the lower the price, the higher the score.

Features Score

We calculate a score between 1 - 10 for each extras treatment category the product offers. 3 factors are scored individually based on their position in the pool, and are averaged to determine the individual score for each extra

The limit associated with the extra,

How many extras is the particular extra combined with, and

The waiting period.

We calculate the score for each extras treatment category after assigning them a pool depending on their position within the assigned pool. The extras treatment categories that are scored are based on the classification of 'core extras' from the Australian government.

We calculate the weighted average for each extras treatment category, based on the product category.

Final Score

The Cost Component scores and Features Component scores are combined and normalised to determine each product's Finder Score.

Why compare health insurance with Finder?

We don't ask for your phone or email to see prices.

With 1 click, you can open your results to nearly every fund in Australia.

You pay the same price as going direct – we charge no fees.

We ask hundreds of Australians what they're paying for extras only health insurance every month. Here's what their bill looked like in July 2024.

Extras only: $73

Price based on 1,000+ responses for single extras insurance.

What's the best extras insurance in Australia?

The extras policies below won 2024 Finder Awards. They came out on top for value for money – meaning they give you more bang for your buck than the other 400+ policies we analysed.

Keep in mind, everyone's needs are different, so it's worth doing some research yourself to get cover that works for you.

This won Finder's Medium Extras cover award in 2023 and 2024. Flex 50 gives you $800 to split how you like across 12 popular services, including dental. You could use all of that $800 combined annual limit on dental if you like, or you could split it up – it's totally up to you.

Finder 2024 health insurer of the year.

Not-for-proft. Profits go back to members, not shareholders.

55.50% of extras treatments covered. One of the best out of 23 funds.

There are cheaper policies but you don't get as much.

Other insurers also offer flex options.

HBF Flex 50 was the winner of our Medium Extras category in the 2024 Finder Awards. It covered more treatments for less money than any other fund.

Consistently one of the cheapest dental insurance policies available. Westfund's Starter Extras option includes general dental cover and an optical benefit up to $180 per person. You can also choose how to spend $400 across a bunch of services including dental, optical, physio, chiro and more.

2024 Finder Award winner in the Core Extras category.

Excellent complaints record.

Not-for-profit.

There are some cheaper options.

This is a basic plan. There are more comprehensive plans.

Westfund Starter was the winner of our Core Extras category in the 2024 Finder Awards. It covered more treatments for less money than any other fund.

There's no way to find the best extras cover for everyone. We all have different circumstances and will use our extras cover for different things. However, the Finder Awards are one way of figuring out which extras policies offer the best value for money. Here's how we chose the winners.

Note: Prices for the products above are based on a single person earning less than $97,000 a year in Sydney.

Best Extras Insurance Awards - Comprehensive/Medium/Core

Products were assessed by weighing their coverage level against the national average price of a singles policy. Coverage level was obtained from by assessing coverage for the 15 treatment categories in the image below. This was compared to the price of each product, with policies offering the best value scoring the highest.

Eligible policies were divided into three tiers: Core, Medium and Comprehensive, based on the criteria below. Policies were only considered for the top category they were eligible for. The policies within each tier were then ranked.

Selection Criteria

The policy must be available for new policy holders as of April 2023

An insurer may only claim one place in the final winners' list in this category

The product must not be from a restricted fund

The product must be approved by the Commonwealth Ombudsman

Funds must have at least 0.5% national market share, according to the Commonwealth Ombudsman

The product must be classed at the appropriate tier for the awards (Comprehensive/Medium/Core)

Extras cover generally includes non-hospital services that aren't covered by Medicare, like dental and optical. The table below outlines some of the most common treatment categories.

Coverage for hearing aid devices and audiology services can be covered. You'll generally only be able to claim for hearing aids every few years (3 to 5 years is common).

Waiting periods for extras cover

Waiting periods for health insurance apply to both extras and hospital policies. You'll generally need to wait for a period of between 2 and 12 months before claiming a particular benefit. Some major treatments require waiting periods of up to 2 or more years but this is less common. A very small handful of insurers let you skip waiting periods.

General dental - 2 months

Optical (e.g. glasses or contact lenses) - 6 months

Major dental (e.g. crowns, bridges) - 12 months

Orthodontics - 1-3 years

I've always taken out a policy that comes with no waiting periods. It means I can start claiming straight away. I once took out extras cover and was able to claim $600 worth of benefits in a week.

Benefit limits for extras only health insurance are the maximum amounts you can claim for specific treatments each calendar year. Many funds also break these down into the following types:

Combined limits. This is where several different services are included in one shared limit, such as physiotherapy, chiropractic and remedial massage all falling under an overall physical therapy benefit.

Sub-limits. These apply to specific treatments under a certain service, such as $500 for dentures and $800 for crowns, even though they fall under a major dental benefit.

Lifetime limits. Fairly rare and generally only applied to orthodontics, this means that your limit does not renew each year, and is carried over even if you switch to a higher level of cover or switch funds.

Set benefits vs percentage benefits

Health funds use two methods to cover extras services. Set benefits apply a fixed amount to each service, such as $500 for general dental, while percentage benefits do what the name suggests and calculates the benefit as a percentage that covers all services, such as 50% back. Some pros and cons of each method are outlined below:

Cover method

Pros

Cons

Set benefits

You can customise your cover by picking a policy that pays the highest benefits for specific services.

Some funds increase the benefits each year that you continue to hold cover as a loyalty bonus.

Harder to calculate your out-of-pocket expenses, unless you know how much the provider charges for your treatment.

Percentage benefits

Provides more certainty as you know whatever the bill is a set percentage of it is covered.

You may be able to opt for a higher percentage back in exchange for paying a slightly higher premium.

No ability to prioritise specific services, since the percentage back applies to everything covered by the policy.

State of the Funds report.'N/A' signifies no activity in that state.

Why you can trust Finder's health insurance experts

You pay nothing. Finder is free to use. And you pay the same as going direct. No markups, no hidden fees.

You save time. We spend 100s of hours researching health insurance so you can sort the gold from the junk faster.

You can trust us. We say it like it is. We aren't owned by an insurer and our opinions are our own.

Frequently asked questions

Extras cover is a type of health insurance that helps you pay for treatments and services such as dental, physio and glasses. These aren't usually covered by Medicare and are typically done out-of-hospital.

We looked at 236 extras policies. At around $12 per month, Bupa Extras Saver offers the cheapest extras insurance cover according to our research. It only covers general dental.

Extras benefits usually reset either on 1 January or 1 July, depending on your insurer. These dates represent the start of the calendar year or the financial year. Occasionally, it may be based on the date you took out your policy, also known as your policy anniversary. You can see details on when each fund resets extras benefits here.

The cost of extras cover varies depending on how comprehensive your policy is. Currently, the average price of a extras policy is $16

per week*. The cost of the cheapest extras policy available today is just $4

per week*.

No, extras insurance will not exempt you from the Medicare Levy Surcharge. For high-earners to be exempt from the MLS you'll need private hospital cover, rather than extras. The hospital policy must have an excess of $750 or less for singles, or $1,500 or less for couples and families.

If you're breaking even in cost, but are going to the dentist and using more health services than before, you're coming out ahead in both health and cost. This is because preventative measures, such as dental cleaning, which is included in many extras policies, mean you're less likely to need more expensive treatments later.

General dental cover, in particular, is one of the stars of any extras policy. It's available with the most inexpensive and basic plans. Some extras policies even cover 100% of the cost of up to two dental checks per year.

Children who have regular dental check-ups in general tend to be at lower risk of oral disease as they get older; and adults can also take advantage of regular checks and professional dental cleaning to help stave off more complex and expensive conditions. Health extras can start delivering benefits almost immediately, but much like other forms of insurance some of the advantages only pay off years later.

No, you will not need to pay an excess on extras health insurance cover. Excesses are only applicable to hospital claims.

How we calculate Health Insurance Extras Finder Scores

Gary Ross Hunter was an editor at Finder, specialising in insurance. He’s been writing about life, travel, home, car, pet and health insurance for over 6 years and regularly appears as an insurance expert in publications including The Sydney Morning Herald, The Guardian and news.com.au. Gary holds a Kaplan Tier 2 General Advice General Insurance certification which meets the requirements of ASIC Regulatory Guide 146 (RG146). See full bio

Gary Ross's expertise

Gary Ross has written 718 Finder guides across topics including:

Tim Bennett is a Finder insurance & utilities expert. For over 10 years he's reported on news, politics, finance and other topics as a journalist and radio presenter. Tim's roles have included radio news reader and breakfast at the ABC, news producer for SBS and producer for Fairfax Media. Tim regularly appears as a health insurance expert on programs like Sunrise and SBS news, as well as in the Australian, The Daily Telegraph, The Courier Mail and more. See full bio

Tim's expertise

Tim has written 118 Finder guides across topics including:

While COVID-19 vaccinations are free in Australia, other vaccines with out-of-pocket costs can be covered by private health insurance with some extras policies.

Remedial massage can help ease pain from general wear and tear as well as specific injuries. This treatment isn’t covered by Medicare but is included in private health insurance extras cover. Find out how private health insurance can cover you for remedial massage therapy.

Physiotherapy services can be beneficial at any life stage, so it could be worth considering and comparing extras health insurance that can cover the cost of this type of treatment.

If you're wondering what pharmaceutical costs are covered by private health insurance, we've got a guide to health cover for non-PBS pharmaceuticals here.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

Important information about this website

finder.com.au is one of Australia's leading comparison websites. We are committed to our readers and stands by our editorial principles

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product. You can learn more about how we make money.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

You pay nothing. Finder is free to use. And you pay the same as going direct. No markups, no hidden fees.

You pay nothing. Finder is free to use. And you pay the same as going direct. No markups, no hidden fees.

You save time. We spend 100s of hours researching health insurance so you can sort the gold from the junk faster.

You save time. We spend 100s of hours researching health insurance so you can sort the gold from the junk faster.

You can trust us. We say it like it is. We aren't owned by an insurer and our opinions are our own.

You can trust us. We say it like it is. We aren't owned by an insurer and our opinions are our own.