These home loans offer low costs, coupled with a host of features, giving the best overall value.

7+

Great

These home loans may have slightly higher interest rates or fewer features but overall, a competitive offering.

5+

Standard

Usually the home loans would offer above average rates. They may still include some competitive features.

0+

Basic

Higher costs and/or fewer features.

Fixed rate home loans with offset accounts let you lock in set mortgage repayments but also get the interest-saving benefits of an offset account. Offset accounts are more common on variable rate loans, and only a few lenders offer them on fixed rates too. Some of the current options are listed below.

Compare fixed rate home loans with offset accounts

{"userFilters":[{"componentType":"MULTI-SELECT CHECKBOX","options":{"comparator":"contains","includeAllSelection":false,"defaultMatcher":"ANY","values":["Owner-occupier","Investor"],"fields":[{"label":"Owner-occupier","value":"Owner-occupier","comparator":"contains"},{"label":"Investor","value":"Investor","comparator":"contains"}]},"dataSelector":{"recordType":"VARIANT","fieldCode":"DETAILS.LOAN_PURPOSE"},"dataType":"TEXT","label":"Loan Purpose","order":0},{"componentType":"MULTI-SELECT CHECKBOX","options":{"comparator":"contains","includeAllSelection":false,"defaultMatcher":"ANY","values":["Fixed","Variable"],"fields":[{"label":"Fixed","value":"Fixed","comparator":"contains"},{"label":"Variable","value":"Variable","comparator":"contains"}]},"dataSelector":{"recordType":"PRODUCT","fieldCode":"DETAILS.PRODUCT_TYPE"},"dataType":"TEXT","label":"Loan type","order":1},{"componentType":"MULTI-SELECT CHECKBOX","options":{"comparator":"contains","includeAllSelection":false,"defaultMatcher":"ANY","values":["5","10","20","30","40"],"fields":[{"label":"less than 5%","value":"5","comparator":"lte"},{"label":"10%","value":"10","comparator":"eq"},{"label":"20%","value":"20","comparator":"eq"},{"label":"30%","value":"30","comparator":"eq"},{"label":"40% or more","value":"40","comparator":"gte"}]},"dataSelector":{"recordType":"VARIANT","fieldCode":"DETAILS.MIN_DEPOSIT"},"dataType":"PERCENTAGE","label":"Min. deposit","order":2},{"componentType":"SINGLE-SELECT CHECKBOX","options":{"fields":[{"label":"Offset account","fieldCode":"FEATURES.MORTGAGE_OFFSET","value":1},{"label":"Redraw facility","fieldCode":"FEATURES.FACILITY_REDRAW","value":1},{"label":"Extra repayments","fieldCode":"FEATURES.EXTRA_PAYMENTS","value":1},{"label":"Cashback","fieldCode":"GENERAL.CASHBACK","value":1},{"label":"Finder award winner","fieldCode":"GENERAL.FINDER_AWARDS_WINNER","value":1}]},"dataSelector":{"recordType":"VARIANT","fieldCode":null},"dataType":null,"label":"Features","order":3},{"componentType":"PROVIDER","options":null,"dataSelector":{"recordType":"PRODUCT","fieldCode":"GENERAL.PROVIDER_ID"},"dataType":"UUID","label":"Lender","order":4}],"niche":{"currencySymbol":"$","decimalPoint":".","decimalPlaces":"2","thousandsSeparator":","},"prefilled":false}

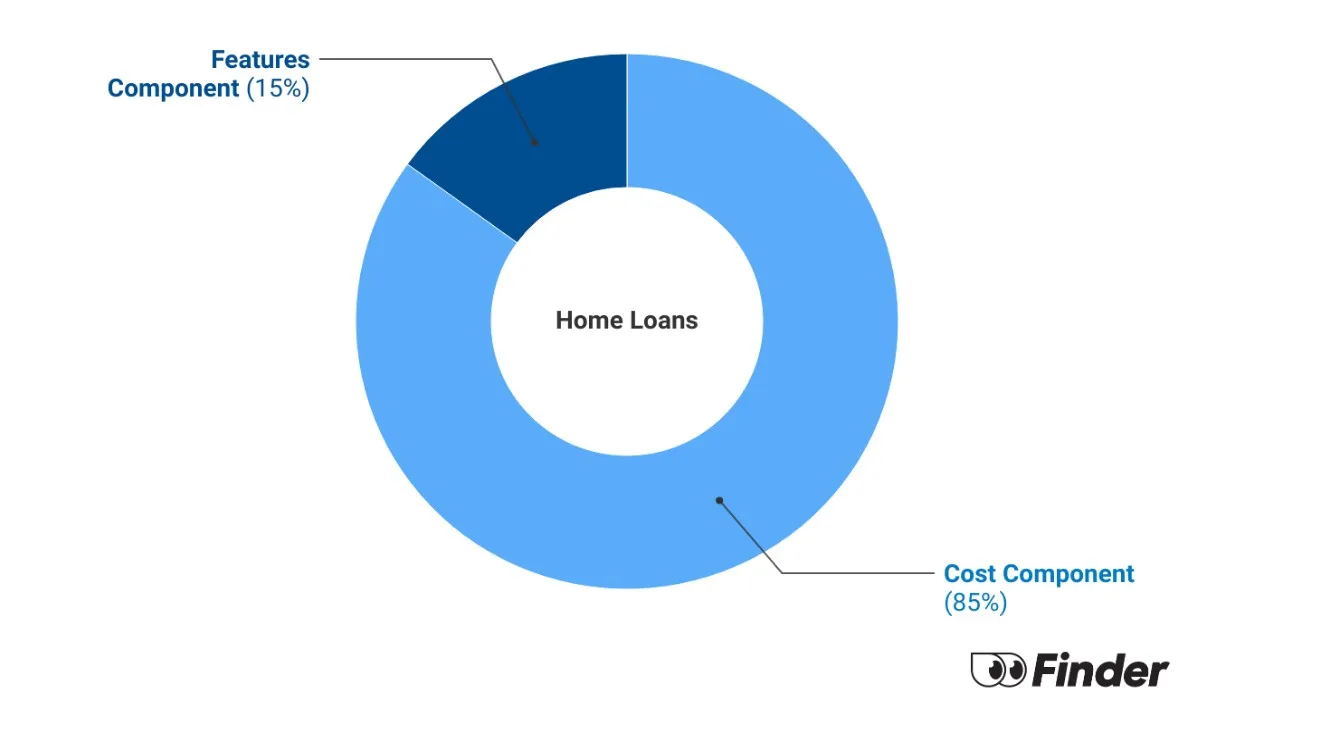

The Finder Score crunches 7,000 home loans across 120+ lenders. It takes into account the product's interest rate, fees and features, as well as the type of loan eg investor, variable, fixed rate - this gives you a simple score out of 10.

To provide a Score, we compare like-for-like loans. So if you're comparing the best home loans for cashback, you can see how each home loan stacks up against other home loans with the same borrower type, rate type and repayment type. We also take into consideration the amount of cashback offered when calculating the Score so you can tell if it's really worth it.

A fixed rate loan with a 100% offset account lets you save money on the interest you pay. The balance of your offset account will offset your principal loan amount, and you don't pay interest on that portion of the loan. Any money you would normally pay as interest is paid towards your home loan principal instead – so you'll actually end up owning your home outright sooner.

Offset accounts are not offered on all fixed rate loans.

Donny’s offset account

Let’s compare 2 scenarios with Donny, our savvy borrower.

In the first example, Donny has a home loan with a rate of 5.0%. His loan size is $500,000 and his repayments are approximately $2,685 a month. He’ll pay a total of $966,279 over the 30 years that he has the loan, $466,279 of which is interest.

If Donny has an offset account and keeps $20,000 in it over the course of his loan, he would pay off his loan 1 year and 10 months earlier and would save $60,011 in interest. That means he'll own his home more than a year earlier, saving a full year of mortgage repayments – all because of a simple offset feature!

His repayments would still be the same, but more of each repayment would go towards the principal (the original loan amount).

Finder survey: How many Australians use an offset account?

Response

Yes

62.69%

No

37.31%

Source: Finder survey by Pure Profile of 1112 Australians, December 2023

How to compare these types of mortgages

Fixed term. Think about how long you want to be locked into the rate. Terms can range from 1 to 10 years. Choose a term you think you’ll be comfortable with, and remember that break fees are payable if you exit your loan before the term ends. If you plan to sell your property in the future, ensure that your fixed term accommodates this.

Fees. These types of loans may come with upfront and ongoing fees that could negate the savings you may make in the long run, so remember to take these into account.

Additional features. As well as an offset account, the home loan may offer you other features, such as a redraw facility, the ability to make additional repayments and discounts. Check to see if you stand to make any further savings.

Sarah Megginson's tip

I usually opt for a split loan of part-fixed and part-variable. I fix around half of my loan for 2-3 years, then keep the rest variable and get an offset account so I can 'offset' the interest. This way, I can choose from a much wider range of home loans and don't have to lock in the full amount as a fixed rate mortgage.

— Sarah Megginson, Finder crew member

Pros and cons of 100% offset accounts

Pros

With a fixed loan, your repayments will remain the same during the fixed interest rate period. If variable rates are increased, you won't pay more.

The balance you have in the offset account will be taken off your principal loan amount, actively helping to reduce the amount of interest you pay.

You can access and spend the money in your offset account at any time.

Cons

You’re unable to refinance during the fixed rate period without paying break costs, which can be expensive.

Offset accounts can come with account-keeping fees, so it's important to check whether the fees will be more than your potential savings.

You don't earn interest on an offset account like you would in a savings account. However, the interest you save on your home loan is usually at a much higher rate.

Frequently asked questions

Yes. The accounts are linked and you can nominate it as your chosen account, but keep in mind this would reduce the balance in your account and affect the interest you pay on your home loan.

No interest will be earned on the balance in your offset account.

Everyone's circumstances are different, so it's important to consider yours when looking at offset accounts. However, offset accounts are usually a key feature to have as part of your home loan as it reduces your monthly repayments all while you continue to save.

Although you won't earn any interest in an offset account, like you would a savings account, the interest you'll save on your home loan is usually at a much higher rate.

Yes, some banks will give you the option of having multiple offset accounts. However, look out for account fees as you may end up paying multiple fees for multiple accounts.

Why you can trust Finder's home loan experts

You pay nothing. Finder is free to use. And you pay the same as going direct. No markups, no hidden fees. Guaranteed.

You save time. We spend 100s of hours researching home loans so you can sort the gold from the junk faster.

You compare more. Our comparison tools bring you cheaper, better home loans from across the market.

Was this content helpful to you?

Thank you for your feedback!

To make sure you get accurate and helpful information, this guide has been edited by David Gregory as part of our fact-checking process.

As an authority on all things personal finance, Sarah Megginson is passionate about helping you save money and make money. She is an editor and money expert with 20 years’ experience and an extensive background in property and finance journalism. Sarah holds ASIC RG146-compliant Tier 1 Generic Knowledge certification, and she's a regular media commentator, appearing weekly on TV (Sunrise, Channel 7 news, Nine news), radio (KIIS FM, Triple M, 3AW, 2GB, 6PR) and in digital and print media. See full bio

Sarah's expertise

Sarah has written 190 Finder guides across topics including:

While getting a 10-year fixed rate home loan might be a good idea if you want to keep your repayments the same over the next decade, you will pay more if interest rates drop.

Thirty year fixed rate home loans are a great way to lock in a great interest rate for the entirety of your loan but Australia doesn’t currently offer this lengthy loan option.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

Important information about this website

finder.com.au is one of Australia's leading comparison websites. We are committed to our readers and stands by our editorial principles

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product. You can learn more about how we make money.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

You pay nothing. Finder is free to use. And you pay the same as going direct. No markups, no hidden fees. Guaranteed.

You pay nothing. Finder is free to use. And you pay the same as going direct. No markups, no hidden fees. Guaranteed.

You save time. We spend 100s of hours researching home loans so you can sort the gold from the junk faster.

You save time. We spend 100s of hours researching home loans so you can sort the gold from the junk faster.

You compare more. Our comparison tools bring you cheaper, better home loans from across the market.

You compare more. Our comparison tools bring you cheaper, better home loans from across the market.